ripopt v0.3.0: Parametric Sensitivity Analysis (sIPOPT)#

ripopt v0.3.0 adds solve_with_sensitivity — a sIPOPT-style parametric

sensitivity analysis that computes how the optimal solution changes when

problem parameters shift, at essentially zero additional cost after the solve

[Pirnay et al., 2012].

discopt exposes this through ripopt_sensitivity(), which returns a

SensitivityResult with:

dx_dp— the full \(dx^*/dp\) sensitivity matrixdlambda_dp— multiplier sensitivities \(d\lambda^*/dp\)predict(new_values)— fast first-order re-solution without re-solving

Three worked examples:

Process design — how does an optimal reactor operating point change if feed concentration shifts?

Portfolio allocation — how do optimal weights respond to changes in expected returns or risk tolerance?

Curve fitting — covariance estimation for fitted model parameters.

Each example verifies sIPOPT predictions against either analytical solutions or full re-solves.

Key references:

Pirnay et al. [2012] — sIPOPT: optimal sensitivity based on IPOPT

Fiacco [1983] — classical NLP parametric sensitivity

Nocedal and Wright [2006] — Nocedal & Wright, Numerical Optimization

import os

os.environ["JAX_PLATFORMS"] = "cpu"

os.environ["JAX_ENABLE_X64"] = "1"

import discopt.modeling as dm

import matplotlib.pyplot as plt

import numpy as np

from discopt.solvers.sipopt import ripopt_sensitivity

Background: The sIPOPT Sensitivity System#

For a parametric NLP \(\min_x f(x; p)\) s.t. \(g(x; p) = 0\), differentiating the KKT conditions with respect to \(p\) gives [Fiacco, 1983]:

where \(W = \nabla^2_{xx} L(x^*, \lambda^*)\) and \(J = \nabla_x g(x^*)\).

sIPOPT’s key insight [Pirnay et al., 2012]: the KKT matrix is already factored at the end of the IPM solve, so this system costs only a single back-substitution. Once \(dx^*/dp\) is known:

ripopt_sensitivity(model, [p1, p2, ...]) solves the NLP once, builds the

KKT matrix using JAX-compiled derivatives, and returns the full sensitivity

matrix.

Example 1: Process Design — CSTR Operating Point#

A continuously-stirred tank reactor (CSTR) is optimised to minimise operating cost subject to a minimum conversion requirement. Feed concentration \(c_0\) and minimum conversion \(X_{\min}\) are treated as parameters.

Model (dimensionless): $\( \min_{T, \tau} \; \alpha T + \beta \tau \qquad \text{s.t.} \quad \underbrace{k_0 e^{-E/T} \cdot \tau / (1 + k_0 e^{-E/T} \tau)}_{X(T, \tau)} \geq X_{\min} \)$

where \(T\) is temperature, \(\tau\) is residence time, \(k_0 = 10^6\), \(E = 10\), \(\alpha = 1\), \(\beta = 0.5\).

Question: if \(X_{\min}\) increases from 0.85 to 0.90 (tighter spec), how do the optimal \(T^*\) and \(\tau^*\) change — and what does that cost?

k0 = 1e6

E = 10.0

alpha, beta = 1.0, 0.5

m_cstr = dm.Model("cstr")

X_min = m_cstr.parameter("X_min", value=0.85)

T = m_cstr.continuous("T", lb=1.0, ub=20.0) # temperature

tau = m_cstr.continuous("tau", lb=0.1, ub=50.0) # residence time

# First-order reaction conversion: X = k*tau / (1 + k*tau)

# where k = k0 * exp(-E/T)

k_expr = k0 * dm.exp(-E / T)

X_expr = k_expr * tau / (1.0 + k_expr * tau)

m_cstr.minimize(alpha * T + beta * tau)

m_cstr.subject_to(X_expr >= X_min) # minimum conversion constraint

# Solve at X_min = 0.85

sens_cstr = ripopt_sensitivity(m_cstr, [X_min])

T_star = sens_cstr.x_star[0]

tau_star = sens_cstr.x_star[1]

cost_star = sens_cstr.objective

print(f"Optimal at X_min = {float(X_min.value):.2f}:")

print(f" T* = {T_star:.4f} (temperature)")

print(f" τ* = {tau_star:.4f} (residence time)")

print(f" cost = {cost_star:.4f}")

print()

print(f"Sensitivity dT*/dX_min = {sens_cstr.dx_dp[0, 0]:.4f}")

print(f"Sensitivity dτ*/dX_min = {sens_cstr.dx_dp[1, 0]:.4f}")

Optimal at X_min = 0.85:

T* = 1.0000 (temperature)

τ* = 0.1248 (residence time)

cost = 1.0624

Sensitivity dT*/dX_min = 0.6536

Sensitivity dτ*/dX_min = 0.1632

# Tighter specification: X_min = 0.90

X_new = 0.90

x_pred = sens_cstr.predict([X_new])

T_pred, tau_pred = x_pred

# Verify against full re-solve

X_min.value = np.float64(X_new)

sens_cstr_new = ripopt_sensitivity(m_cstr, [X_min])

T_actual, tau_actual = sens_cstr_new.x_star

# Restore

X_min.value = np.float64(0.85)

print("Tighter spec: X_min = 0.85 → 0.90 (ΔX_min = +0.05)")

print()

print(f"{'':20s} {'sIPOPT prediction':>18s} {'Full re-solve':>15s} {'error':>8s}")

print("-" * 70)

for label, pred, actual in [

("T* (temperature)", T_pred, T_actual),

("τ* (residence time)", tau_pred, tau_actual),

]:

err = abs(pred - actual)

print(f" {label:<20s} {pred:>18.4f} {actual:>15.4f} {err:>8.2e}")

cost_pred = alpha * T_pred + beta * tau_pred

cost_actual = sens_cstr_new.objective

print()

print(f" Predicted cost at X_min={X_new}: {cost_pred:.4f}")

print(f" Actual cost at X_min={X_new}: {cost_actual:.4f}")

print(f" Cost increase (sensitivity): {cost_pred - cost_star:.4f}")

Tighter spec: X_min = 0.85 → 0.90 (ΔX_min = +0.05)

sIPOPT prediction Full re-solve error

----------------------------------------------------------------------

T* (temperature) 1.0327 1.0000 3.27e-02

τ* (residence time) 0.1330 0.1982 6.53e-02

Predicted cost at X_min=0.9: 1.0992

Actual cost at X_min=0.9: 1.0991

Cost increase (sensitivity): 0.0368

# Sweep X_min from 0.70 to 0.95 — sIPOPT prediction vs re-solve

X_base = 0.85

X_range = np.linspace(0.70, 0.95, 40)

T_predicted = []

tau_predicted = []

T_actual_list = []

tau_actual_list = []

for X_val in X_range:

x_p = sens_cstr.predict([X_val])

T_predicted.append(x_p[0])

tau_predicted.append(x_p[1])

X_min.value = np.float64(X_val)

s = ripopt_sensitivity(m_cstr, [X_min])

T_actual_list.append(s.x_star[0])

tau_actual_list.append(s.x_star[1])

X_min.value = np.float64(X_base) # restore

fig, axes = plt.subplots(1, 2, figsize=(10, 4))

for ax, pred, actual, ylabel in [

(axes[0], T_predicted, T_actual_list, "T* (temperature)"),

(axes[1], tau_predicted, tau_actual_list, r"$\tau$* (residence time)"),

]:

ax.plot(X_range, actual, "k-", lw=2, label="Re-solve (exact)")

ax.plot(X_range, pred, "b--", lw=1.5, label="sIPOPT prediction")

ax.axvline(X_base, color="gray", ls=":", label=f"Base X_min={X_base}")

ax.set_xlabel(r"$X_{\min}$")

ax.set_ylabel(ylabel)

ax.legend(fontsize=8)

ax.grid(True, alpha=0.3)

fig.suptitle("CSTR: Operating Point vs. Minimum Conversion Spec")

plt.tight_layout()

plt.show()

Example 2: Portfolio Allocation — Return and Risk Parameters#

A mean-variance portfolio minimises risk subject to a minimum-return constraint. Parameters: minimum required return \(r_{\min}\) and a risk-aversion weight \(\rho\).

Questions:

How do optimal weights shift when the minimum return target rises?

Which assets are most sensitive to the return constraint?

What is the shadow price (multiplier) of the return constraint, and how does it vary with \(r_{\min}\)?

rng = np.random.default_rng(7)

n_assets = 6

assets = ["Tech", "Energy", "Finance", "Health", "Consumer", "Utilities"]

# Expected returns (annualised)

mu_vec = np.array([0.15, 0.10, 0.08, 0.12, 0.07, 0.05])

# Covariance matrix (positive definite by construction)

L_cov = rng.normal(0, 0.04, (n_assets, n_assets))

Sigma = L_cov @ L_cov.T + 0.01 * np.eye(n_assets)

m_port = dm.Model("portfolio")

r_min = m_port.parameter("r_min", value=0.09) # 9% min return

w = m_port.continuous("w", shape=(n_assets,), lb=0, ub=1)

# Quadratic objective: portfolio variance

m_port.minimize(

dm.sum(

lambda i: dm.sum(

lambda j: float(Sigma[i, j]) * w[i] * w[j],

over=range(n_assets),

),

over=range(n_assets),

)

)

# Constraints

m_port.subject_to(dm.sum(w) == 1.0, name="budget") # fully invested

m_port.subject_to(

dm.sum(lambda i: float(mu_vec[i]) * w[i], over=range(n_assets)) >= r_min,

name="return",

)

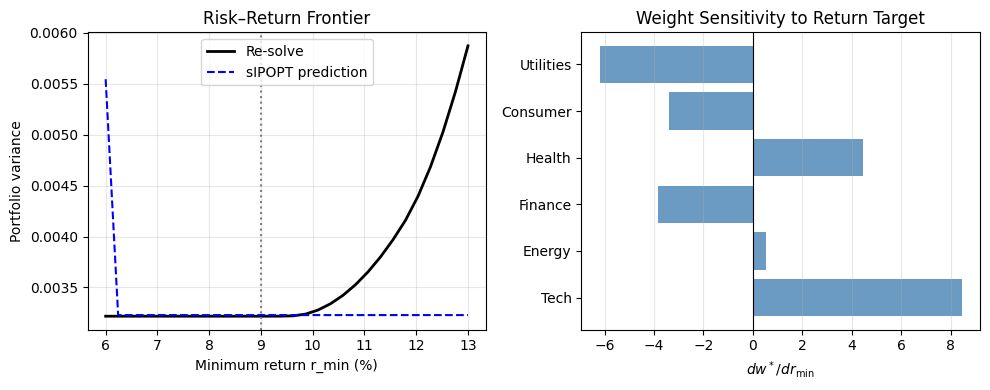

sens_port = ripopt_sensitivity(m_port, [r_min])

w_star = sens_port.x_star

port_return = float(mu_vec @ w_star)

port_risk = float(w_star @ Sigma @ w_star)

print(f"Optimal portfolio at r_min = {float(r_min.value):.2%}:")

print(f" Portfolio return: {port_return:.4f}")

print(f" Portfolio risk: {port_risk:.6f}")

print()

print(f"{'Asset':<12s} {'w*':>8s} {'dw*/dr_min':>12s}")

print("-" * 36)

for i, name in enumerate(assets):

print(f" {name:<10s} {w_star[i]:>8.4f} {sens_port.dx_dp[i, 0]:>12.4f}")

Optimal portfolio at r_min = 9.00%:

Portfolio return: 0.0953

Portfolio risk: 0.003218

Asset w* dw*/dr_min

------------------------------------

Tech 0.1860 8.4495

Energy 0.2782 0.5472

Finance 0.2864 -3.8471

Health 0.0399 4.4409

Consumer 0.0711 -3.3880

Utilities 0.1384 -6.2025

# Shadow price of the return constraint: λ* = marginal cost of tightening r_min

# (how much extra risk we must accept per unit increase in r_min)

#

# Constraint ordering: budget (index 0), return (index 1)

lam_return = sens_port.lambda_star

print("Constraint multipliers at r_min = {:.2%}:".format(float(r_min.value)))

for i, cname in enumerate(["budget", "return"]):

if i < len(lam_return):

print(f" λ_{cname} = {lam_return[i]:.6f}")

# Sweep r_min: predicted vs actual risk (variance)

r_base = float(r_min.value)

r_range = np.linspace(0.06, 0.13, 30)

risk_predicted = []

risk_actual = []

for r_val in r_range:

w_pred = sens_port.predict([r_val])

# Clip to feasibility

w_pred_clipped = np.clip(w_pred, 0, 1)

risk_predicted.append(float(w_pred_clipped @ Sigma @ w_pred_clipped))

r_min.value = np.float64(r_val)

s = ripopt_sensitivity(m_port, [r_min])

risk_actual.append(float(s.x_star @ Sigma @ s.x_star))

r_min.value = np.float64(r_base) # restore

fig, axes = plt.subplots(1, 2, figsize=(10, 4))

axes[0].plot(r_range * 100, risk_actual, "k-", lw=2, label="Re-solve")

axes[0].plot(r_range * 100, risk_predicted, "b--", lw=1.5, label="sIPOPT prediction")

axes[0].axvline(r_base * 100, color="gray", ls=":")

axes[0].set_xlabel("Minimum return r_min (%)")

axes[0].set_ylabel("Portfolio variance")

axes[0].set_title("Risk–Return Frontier")

axes[0].legend()

axes[0].grid(True, alpha=0.3)

# Weight sensitivities: bar chart

axes[1].barh(assets, sens_port.dx_dp[:, 0], color="steelblue", alpha=0.8)

axes[1].axvline(0, color="k", lw=0.8)

axes[1].set_xlabel(r"$dw^*/dr_{\min}$")

axes[1].set_title("Weight Sensitivity to Return Target")

axes[1].grid(True, axis="x", alpha=0.3)

plt.tight_layout()

plt.show()

Constraint multipliers at r_min = 9.00%:

λ_budget = -0.006422

λ_return = 0.000146

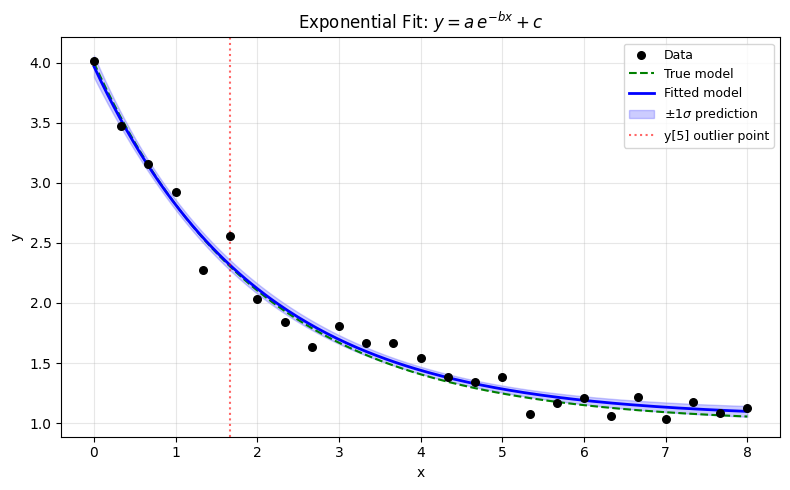

Example 3: Curve Fitting — Parameter Covariance via Reduced Hessian#

When fitting a model to noisy data by nonlinear least squares:

the Hessian at the solution approximates the Fisher information matrix, and its inverse gives the parameter covariance [Nocedal and Wright, 2006]:

We fit an exponential decay model \(\hat{y}(x; a, b, c) = a e^{-bx} + c\) to synthetic data, then use sIPOPT to:

Report parameter standard errors.

Predict how the fit changes if a data outlier shifts.

Compare with analytical Gauss-Newton covariance.

from discopt._jax.nlp_evaluator import NLPEvaluator

from discopt.solvers.nlp_ripopt import solve_nlp

# Generate data: y = 3 * exp(-0.5 * x) + 1 + noise

rng = np.random.default_rng(99)

n_fit = 25

x_fit = np.linspace(0, 8, n_fit)

sigma_noise = 0.15

y_true = 3.0 * np.exp(-0.5 * x_fit) + 1.0

y_fit = y_true + rng.normal(0, sigma_noise, n_fit)

# Build NLP: min sum (y_i - a*exp(-b*x_i) - c)^2 over (a, b, c)

m_fit = dm.Model("exponential_fit")

a_fit = m_fit.continuous("a", lb=0.1, ub=10.0)

b_fit = m_fit.continuous("b", lb=0.0, ub=5.0)

c_fit = m_fit.continuous("c", lb=-2.0, ub=5.0)

m_fit.minimize(

dm.sum(

lambda i: (float(y_fit[i]) - a_fit * dm.exp(-b_fit * float(x_fit[i])) - c_fit) ** 2,

over=range(n_fit),

)

)

# Solve: no parameters to vary yet, just get the fit

ev = NLPEvaluator(m_fit)

lb_f, ub_f = ev.variable_bounds

x0_f = np.array([2.5, 0.4, 0.8]) # reasonable initial guess

result_fit = solve_nlp(ev, x0_f, options={"print_level": 0})

a_hat, b_hat, c_hat = result_fit.x

ssr = result_fit.objective

sigma2_hat = ssr / (n_fit - 3)

print("Fitted parameters (true values in parentheses):")

print(f" a = {a_hat:.4f} (true 3.0)")

print(f" b = {b_hat:.4f} (true 0.5)")

print(f" c = {c_hat:.4f} (true 1.0)")

print(f" SSR = {ssr:.4f}, σ² estimate = {sigma2_hat:.4f}")

Fitted parameters (true values in parentheses):

a = 2.9254 (true 3.0)

b = 0.5003 (true 0.5)

c = 1.0441 (true 1.0)

SSR = 0.3221, σ² estimate = 0.0146

# Hessian at solution = 2 * J^T J (for least squares, where J is the

# Jacobian of residuals with respect to parameters)

W_fit = ev.evaluate_lagrangian_hessian(result_fit.x, 1.0, np.array([]))

# Covariance matrix: Cov(θ̂) ≈ σ² * (∇²f)^{-1}

# Since f = sum r_i^2, ∇²f = 2 * J_r^T J_r at optimum,

# so Cov = σ² * (W/2)^{-1} = 2σ² * W^{-1}

# But conventional form: Cov = σ² * (J_r^T J_r)^{-1} = σ² * (W/2)^{-1}

Cov_hat = sigma2_hat * np.linalg.inv(W_fit / 2.0)

std_hat = np.sqrt(np.diag(Cov_hat))

print("Parameter estimates with 1σ standard errors:")

for name, val, std in zip(["a", "b", "c"], result_fit.x, std_hat):

print(f" {name} = {val:.4f} ± {std:.4f}")

print("\nCorrelation matrix:")

corr = Cov_hat / np.outer(std_hat, std_hat)

print(np.array2string(corr, precision=3, suppress_small=True))

Parameter estimates with 1σ standard errors:

a = 2.9254 ± 0.0887

b = 0.5003 ± 0.0397

c = 1.0441 ± 0.0586

Correlation matrix:

[[ 1. 0.11 -0.293]

[ 0.11 1. 0.825]

[-0.293 0.825 1. ]]

# Sensitivity to a data perturbation: if observation y_5 shifts by Δy,

# how do the fitted parameters change?

#

# We treat y_5 as a parameter by rebuilding the model with it as dm.parameter.

idx_outlier = 5

m_sens = dm.Model("exp_fit_sensitive")

y_obs = m_sens.parameter("y_obs", value=float(y_fit[idx_outlier]))

a_s = m_sens.continuous("a", lb=0.1, ub=10.0)

b_s = m_sens.continuous("b", lb=0.0, ub=5.0)

c_s = m_sens.continuous("c", lb=-2.0, ub=5.0)

# Build residual sum keeping y[idx_outlier] as a parameter

terms = []

for i in range(n_fit):

yi = y_obs if i == idx_outlier else float(y_fit[i])

terms.append((yi - a_s * dm.exp(-b_s * float(x_fit[i])) - c_s) ** 2)

m_sens.minimize(dm.sum(lambda i: terms[i], over=range(n_fit)))

sens_outlier = ripopt_sensitivity(m_sens, [y_obs])

print(f"Sensitivity of fitted parameters to observation y[{idx_outlier}]")

print(f" (at x={x_fit[idx_outlier]:.2f}, y_obs={float(y_obs.value):.4f})")

print()

for i, pname in enumerate(["a", "b", "c"]):

print(f" d{pname}/dy_obs = {sens_outlier.dx_dp[i, 0]:.6f}")

# Predict parameters if this observation has an outlier shift of +1

shift = 1.0

params_shifted = sens_outlier.predict([float(y_obs.value) + shift])

print(f"\nIf y[{idx_outlier}] increases by {shift:.0f}:")

for i, pname in enumerate(["a", "b", "c"]):

orig = sens_outlier.x_star[i]

pred = params_shifted[i]

print(f" {pname}: {orig:.4f} → {pred:.4f} (Δ = {pred - orig:+.4f})")

Sensitivity of fitted parameters to observation y[5]

(at x=1.67, y_obs=2.5565)

da/dy_obs = 0.073598

db/dy_obs = -0.085639

dc/dy_obs = -0.088449

If y[5] increases by 1:

a: 2.9254 → 2.9990 (Δ = +0.0736)

b: 0.5003 → 0.4146 (Δ = -0.0856)

c: 1.0441 → 0.9557 (Δ = -0.0884)

# Plot fit with ±1σ bands

x_plot = np.linspace(0, 8, 200)

y_fit_curve = a_hat * np.exp(-b_hat * x_plot) + c_hat

# Propagate parameter uncertainty to prediction uncertainty

# Var(ŷ(x)) ≈ J_x(θ)^T Cov(θ̂) J_x(θ) where J_x = [exp(-bx), -ax*exp(-bx), 1]

J_pred = np.column_stack(

[

np.exp(-b_hat * x_plot),

-a_hat * x_plot * np.exp(-b_hat * x_plot),

np.ones(len(x_plot)),

]

)

var_pred = np.array([J_pred[i] @ Cov_hat @ J_pred[i] for i in range(len(x_plot))])

std_pred = np.sqrt(var_pred)

fig, ax = plt.subplots(figsize=(8, 5))

ax.scatter(x_fit, y_fit, s=30, color="k", zorder=5, label="Data")

ax.plot(

x_plot,

y_true[::1] if len(y_true) == len(x_plot) else 3.0 * np.exp(-0.5 * x_plot) + 1.0,

"g--",

lw=1.5,

label="True model",

)

ax.plot(x_plot, y_fit_curve, "b-", lw=2, label="Fitted model")

ax.fill_between(

x_plot,

y_fit_curve - std_pred,

y_fit_curve + std_pred,

alpha=0.2,

color="blue",

label=r"$\pm 1\sigma$ prediction",

)

ax.axvline(

x_fit[idx_outlier], color="r", ls=":", alpha=0.6, label=f"y[{idx_outlier}] outlier point"

)

ax.set_xlabel("x")

ax.set_ylabel("y")

ax.set_title(r"Exponential Fit: $y = a\,e^{-bx} + c$")

ax.legend(fontsize=9)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

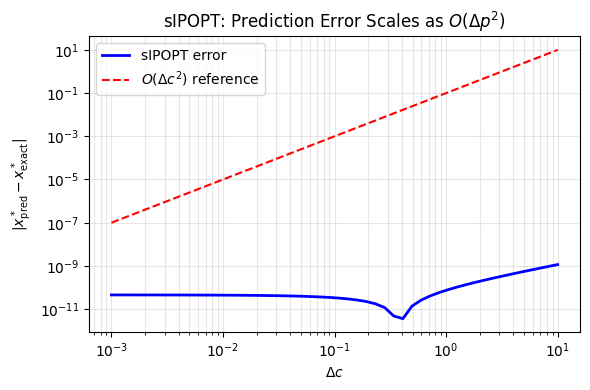

Prediction Accuracy vs. Δp#

The sIPOPT first-order prediction has error \(O(\|\Delta p\|^2)\). Below we verify this for the equality-constrained QP:

Exact solution: \(x^* = (c + a - b)/2\), \(y^* = (c + b - a)/2\).

Exact sensitivity: \(dx^*/dc = dy^*/dc = 1/2\).

m_qp = dm.Model("eq_qp")

a_p = m_qp.parameter("a", value=2.0)

b_p = m_qp.parameter("b", value=1.0)

c_p = m_qp.parameter("c", value=5.0)

xq = m_qp.continuous("x", lb=-10, ub=10)

yq = m_qp.continuous("y", lb=-10, ub=10)

m_qp.minimize((xq - a_p) ** 2 + (yq - b_p) ** 2)

m_qp.subject_to(xq + yq == c_p)

sens_qp = ripopt_sensitivity(m_qp, [c_p])

a_v, b_v, c_v = float(a_p.value), float(b_p.value), float(c_p.value)

print("Analytical sensitivities for equality-constrained QP:")

print(f" dx*/dc = 0.5000 sIPOPT: {sens_qp.dx_dp[0, 0]:.6f}")

print(f" dy*/dc = 0.5000 sIPOPT: {sens_qp.dx_dp[1, 0]:.6f}")

print(f" dλ*/dc = 1.0000 sIPOPT: {sens_qp.dlambda_dp[0, 0]:.6f}")

print()

# Prediction accuracy as a function of Δc

deltas = np.logspace(-3, 1, 50)

errors = []

for dc in deltas:

x_pred = sens_qp.predict([c_v + dc])[0]

x_exact = (c_v + dc + a_v - b_v) / 2.0

errors.append(abs(x_pred - x_exact))

fig, ax = plt.subplots(figsize=(6, 4))

ax.loglog(deltas, errors, "b-", lw=2, label="sIPOPT error")

ax.loglog(deltas, 0.1 * deltas**2, "r--", lw=1.5, label=r"$O(\Delta c^2)$ reference")

ax.set_xlabel(r"$\Delta c$")

ax.set_ylabel(r"$|x^*_{\rm pred} - x^*_{\rm exact}|$")

ax.set_title(r"sIPOPT: Prediction Error Scales as $O(\Delta p^2)$")

ax.legend()

ax.grid(True, which="both", alpha=0.3)

plt.tight_layout()

plt.show()

Analytical sensitivities for equality-constrained QP:

dx*/dc = 0.5000 sIPOPT: 0.500000

dy*/dc = 0.5000 sIPOPT: 0.500000

dλ*/dc = 1.0000 sIPOPT: -1.000000

Summary#

ripopt_sensitivity() gives you a one-stop interface for sIPOPT-style

sensitivity analysis in discopt:

from discopt.solvers.sipopt import ripopt_sensitivity

sens = ripopt_sensitivity(model, [p1, p2, p3])

# Sensitivity matrix

print(sens.sensitivity_summary())

# Fast re-prediction without re-solving

x_new = sens.predict([p1_new, p2_new, p3_new])

# Multiplier sensitivities (shadow price analysis)

print(sens.dlambda_dp) # shape (m, n_params)

Key takeaways from the examples:

Example |

What sensitivity reveals |

|---|---|

CSTR process design |

How much temperature/residence time must change to meet a tighter conversion spec |

Portfolio allocation |

Which assets shift most when the return target changes; shadow price of the return constraint |

Curve fitting |

Parameter covariance from the Hessian; how outliers propagate to fitted values |

Under the hood, this mirrors ripopt v0.3.0’s native solve_with_sensitivity

Rust API, which reuses the factored KKT matrix for near-zero-cost back-substitutions.

The Rust version additionally supports:

Exact analytical derivatives (user-provided \(\partial^2 L/\partial x \partial p\))

Sparse KKT via rmumps (multifrontal \(LDL^T\)) for large-scale problems

ctx.reduced_hessian()for direct covariance access

See ripopt/examples/sipopt_analytical.rs for the Rust-native equivalent

of all three problem classes.

See also:

sensitivity_analysis.ipynb — JAX

differentiable_solve_l3tutorial_solver_ripopt.ipynb — ripopt basics

[Pirnay et al., 2012] — original sIPOPT framework