Decision-Focused Learning with discopt#

Decision-focused learning (DFL) trains a predictive model by backpropagating through an optimization layer [Elmachtoub and Grigas, 2022, Wilder et al., 2019]. Instead of minimizing prediction error (MSE), we minimize decision regret — the gap between the cost of the decision made with predicted parameters and the cost of the decision made with true parameters.

This is a fundamentally different training paradigm:

Approach |

Loss function |

Optimizes for |

|---|---|---|

Two-stage (predict-then-optimize) |

MSE on parameters |

Prediction accuracy |

Decision-focused (end-to-end) |

Decision regret |

Decision quality |

The key insight: a model that is slightly wrong in a way that doesn’t affect decisions is better than a model that is slightly less wrong but makes worse decisions. DFL achieves this by differentiating through the solver [Agrawal et al., 2019, Amos and Kolter, 2017].

What this notebook demonstrates#

A parametric resource allocation problem where costs depend on uncertain features

Training a linear prediction model with standard MSE (two-stage)

Training the same model with decision-focused learning via discopt’s

differentiable_solve_l3(L3 implicit differentiation of KKT conditions)Comparing decision quality: DFL achieves lower regret despite higher prediction error

Prerequisites#

Familiar with the differentiable optimization API from

notebooks/advanced_features.ipynbBasic understanding of gradient descent

import os

os.environ["JAX_PLATFORMS"] = "cpu"

os.environ["JAX_ENABLE_X64"] = "1"

import discopt.modeling as dm

import numpy as np

np.random.seed(42)

print("discopt loaded successfully")

discopt loaded successfully

1. Problem Setup: Parametric Resource Allocation#

A facility must allocate resources \(x_1, x_2, x_3\) to three activities. The cost per unit of each activity depends on external conditions (weather, demand, market prices) captured by a feature vector \(\phi \in \mathbb{R}^5\).

The allocator is risk-averse, penalizing concentrated positions with a quadratic term:

The regularization \(\varepsilon = 1.0\) encourages diversification and makes the optimal allocation a smooth function of the cost parameters — critical for gradient-based learning.

The true costs are a nonlinear function of features (with interactions and noise): $\(c_\text{true}(\phi) = W_\text{true} \, \phi + W_\text{nl} \circ (\phi \otimes \phi) + \epsilon\)$

However, we use a linear predictive model \(\hat{c}(\phi; \theta) = \theta \, \phi\). This model misspecification means the MSE-optimal predictor is not necessarily the best predictor for decisions — creating an opportunity for DFL to outperform.

# Problem dimensions

n_activities = 3

n_features = 5

n_train = 30

n_test = 15

noise_std = 0.15

# Regularization: penalizes concentrated allocations (risk aversion).

# Must be large enough to keep solutions in the interior of [0, 1]

# so that the sensitivity matrix dx*/dc is well-defined everywhere.

eps_reg = 1.0

# True (unknown) cost model: c = W_true @ phi + nonlinear_interactions + noise

# Scaled so cost differences stay moderate relative to eps_reg

W_true = np.array(

[

[0.4, -0.2, 0.1, 0.0, 0.3], # activity 1 costs

[0.0, 0.2, -0.1, 0.4, 0.0], # activity 2 costs

[-0.2, 0.1, 0.2, -0.2, 0.4], # activity 3 costs

]

)

def generate_data(n_samples):

features = np.random.randn(n_samples, n_features)

# Linear part

costs = features @ W_true.T

# Nonlinear interactions that a linear model CANNOT capture.

# These create systematic prediction errors that affect decisions.

costs[:, 0] += 0.4 * features[:, 0] * features[:, 1] # interaction for activity 1

costs[:, 1] += 0.4 * features[:, 2] * features[:, 3] # interaction for activity 2

costs[:, 2] += 0.4 * features[:, 0] * features[:, 4] # interaction for activity 3

# Noise

costs += noise_std * np.random.randn(n_samples, n_activities)

# Center around 1.0 so costs are positive and close together

costs = costs - costs.mean(axis=1, keepdims=True) + 1.0

return features, costs

train_features, train_costs = generate_data(n_train)

test_features, test_costs = generate_data(n_test)

print(f"Training samples: {n_train}")

print(f"Test samples: {n_test}")

print(f"Feature dim: {n_features}")

print(f"Activities: {n_activities}")

print(f"Regularization: eps_reg = {eps_reg}")

print(f"\nSample true costs: {train_costs[0].round(3)}")

print(f"Cost range: [{train_costs.min():.2f}, {train_costs.max():.2f}]")

print(f"Cost spread (max-min per sample): {(train_costs.max(1) - train_costs.min(1)).mean():.2f}")

Training samples: 30

Test samples: 15

Feature dim: 5

Activities: 3

Regularization: eps_reg = 1.0

Sample true costs: [1.01 1.742 0.248]

Cost range: [-0.70, 2.26]

Cost spread (max-min per sample): 1.14

2. Oracle: Optimal Decisions with True Costs#

First, let’s compute the oracle — the best possible decisions when we know the true costs. This gives us a lower bound on achievable cost.

def solve_allocation(cost_vector):

"""Solve the risk-averse resource allocation QP."""

m = dm.Model("allocation")

x = m.continuous("x", shape=(n_activities,), lb=0.0, ub=1.0)

c = m.parameter("cost", value=np.asarray(cost_vector, dtype=np.float64))

# Same regularized QP used everywhere: oracle, two-stage, and DFL

m.minimize(dm.sum(c * x) + eps_reg * dm.sum(x * x))

m.subject_to(dm.sum(x) == 1.0)

result = m.solve()

return np.array([result.x["x"][i] for i in range(n_activities)])

def true_cost(decision, cost_vector):

"""Compute the actual cost of a decision under true costs."""

return float(np.dot(cost_vector, decision))

# Compute oracle decisions and costs on test set

oracle_costs = []

for i in range(n_test):

x_oracle = solve_allocation(test_costs[i])

oracle_costs.append(true_cost(x_oracle, test_costs[i]))

oracle_costs = np.array(oracle_costs)

print(f"Oracle average cost: {oracle_costs.mean():.4f}")

print(f"Oracle cost range: [{oracle_costs.min():.4f}, {oracle_costs.max():.4f}]")

Oracle average cost: 0.5058

Oracle cost range: [-0.7039, 0.9834]

3. Two-Stage Approach: Predict, Then Optimize#

The standard predict-then-optimize approach [Elmachtoub and Grigas, 2022]:

Predict: Train \(\hat{c}(\phi; \theta) = \theta \, \phi\) to minimize MSE on observed costs

Optimize: Plug \(\hat{c}\) into the LP and solve

The prediction model is trained independently of how its predictions will be used.

# Train a linear model with MSE loss: theta @ features -> predicted costs

# Closed-form solution: theta = (X^T X)^{-1} X^T Y

X = train_features # (n_train, n_features)

Y = train_costs # (n_train, n_activities)

theta_mse = np.linalg.lstsq(X, Y, rcond=None)[0].T # (n_activities, n_features)

# Evaluate prediction quality

pred_costs_train = train_features @ theta_mse.T

pred_costs_test = test_features @ theta_mse.T

mse_train = np.mean((pred_costs_train - train_costs) ** 2)

mse_test = np.mean((pred_costs_test - test_costs) ** 2)

print("Two-stage model (MSE-trained):")

print(f" Train MSE: {mse_train:.4f}")

print(f" Test MSE: {mse_test:.4f}")

Two-stage model (MSE-trained):

Train MSE: 0.8664

Test MSE: 1.4504

# Evaluate decision quality on the test set

two_stage_costs = []

for i in range(n_test):

# Decide using predicted costs

x_pred = solve_allocation(pred_costs_test[i])

# Evaluate under true costs

two_stage_costs.append(true_cost(x_pred, test_costs[i]))

two_stage_costs = np.array(two_stage_costs)

two_stage_regret = two_stage_costs - oracle_costs

print("Two-stage decision quality:")

print(f" Average cost: {two_stage_costs.mean():.4f}")

print(f" Average regret: {two_stage_regret.mean():.4f}")

print(f" Max regret: {two_stage_regret.max():.4f}")

Two-stage decision quality:

Average cost: 0.6545

Average regret: 0.1486

Max regret: 0.8628

4. Decision-Focused Learning: End-to-End Training#

Now we train \(\theta\) by backpropagating through the optimization solver [Mandi et al., 2020, Wilder et al., 2019]. The pipeline:

The loss for a single sample is the true cost of the decision made with predicted parameters: $\(\mathcal{L}(\theta) = c_\text{true}^\top x^*(\hat{c}(\phi; \theta))\)$

The gradient flows backward through the solver using discopt’s L3 implicit differentiation [Amos and Kolter, 2017, Fiacco, 1983]:

Solve the QP with predicted costs \(\hat{c}\) to get \(x^*(\hat{c})\) and dual variables

Differentiate the KKT conditions to get \(\frac{dx^*}{d\hat{c}}\) (the sensitivity matrix)

Chain rule: \(\frac{d\mathcal{L}}{d\theta} = \frac{d\mathcal{L}}{dx^*} \cdot \frac{dx^*}{d\hat{c}} \cdot \frac{d\hat{c}}{d\theta}\)

Why regularization matters: We add a quadratic term \(\varepsilon\|x\|^2\) (with \(\varepsilon = 1.0\)) to convert the LP into a smooth QP. Without sufficient regularization, the LP solution sits at a vertex (variables at bounds), the active set is degenerate, and \(dx^*/d\hat{c} = 0\) — no gradient flows! The regularization must be large enough to keep all variables in the interior of [0, 1], ensuring a well-conditioned KKT system and non-trivial sensitivities.

from discopt._jax.differentiable import differentiable_solve_l3

# Build a regularized model for DFL training.

# eps_reg must be large enough to keep all x_i in the interior of [0, 1].

# With costs centered at 1.0 and spread ~0.8, eps_reg=1.0 gives interior solutions.

# (Too small, e.g. 0.01, and the solution hits bounds -> dx*/dc = 0 -> no gradient!)

eps_reg = 1.0

m_dfl = dm.Model("dfl_allocation")

x_dfl_var = m_dfl.continuous("x", shape=(n_activities,), lb=0.0, ub=1.0)

c_dfl_param = m_dfl.parameter("cost", value=np.ones(n_activities, dtype=np.float64))

m_dfl.minimize(dm.sum(c_dfl_param * x_dfl_var) + eps_reg * dm.sum(x_dfl_var * x_dfl_var))

m_dfl.subject_to(dm.sum(x_dfl_var) == 1.0)

# Verify: solve and check that L3 succeeds with non-trivial sensitivity

c_dfl_param.value = np.array([0.8, 1.0, 1.2], dtype=np.float64)

result_demo = differentiable_solve_l3(m_dfl)

x_star = np.array([result_demo.x["x"][i] for i in range(n_activities)])

print("Solve with costs [0.8, 1.0, 1.2]:")

print(f" x* = {x_star.round(4)} (all interior — good for L3!)")

print(f" obj = {result_demo.objective:.4f}")

print(f" L3 status: {'ok' if not result_demo._l3_failed else 'FAILED'}")

sm = result_demo.sensitivity_matrix()

if sm is not None:

print(f"\nSensitivity matrix dx*/dc (shape {sm.shape}):")

print(np.array2string(sm, precision=4, suppress_small=True))

print("\nRows = allocations (x1, x2, x3), Cols = cost parameters (c1, c2, c3)")

print("Diagonal: increasing a cost pushes allocation away from that activity.")

print("Off-diagonal: freed allocation shifts to the other activities.")

else:

print("\nWARNING: sensitivity_matrix is None — L3 failed!")

******************************************************************************

This program contains Ipopt, a library for large-scale nonlinear optimization.

Ipopt is released as open source code under the Eclipse Public License (EPL).

For more information visit https://github.com/coin-or/Ipopt

******************************************************************************

Solve with costs [0.8, 1.0, 1.2]:

x* = [0.4333 0.3333 0.2333] (all interior — good for L3!)

obj = 1.3133

L3 status: ok

Sensitivity matrix dx*/dc (shape (3, 3)):

[[-0.3333 0.1667 0.1667]

[ 0.1667 -0.3333 0.1667]

[ 0.1667 0.1667 -0.3333]]

Rows = allocations (x1, x2, x3), Cols = cost parameters (c1, c2, c3)

Diagonal: increasing a cost pushes allocation away from that activity.

Off-diagonal: freed allocation shifts to the other activities.

# Decision-focused training loop using L3 implicit differentiation.

#

# For each sample (phi, c_true):

# 1. Predict costs: c_hat = theta @ phi

# 2. Solve regularized QP with c_hat -> get x*(c_hat) and dx*/dc via L3

# 3. Compute loss = c_true @ x*(c_hat)

# 4. Chain rule: d(loss)/d(theta[j,k]) = (dx*/dc^T @ c_true)[j] * phi[k]

# 5. Gradient descent on theta

theta_dfl = theta_mse.copy() # warm start from MSE solution

learning_rate = 0.05

n_epochs = 10

batch_size = 10

print(f"Starting DFL training: {n_epochs} epochs, lr={learning_rate}, batch={batch_size}")

print(f"Theta shape: {theta_dfl.shape}")

print()

dfl_losses = []

for epoch in range(n_epochs):

perm = np.random.permutation(n_train)

epoch_loss = 0.0

n_batches = 0

n_l3_ok = 0

n_l3_total = 0

for start in range(0, n_train, batch_size):

idx = perm[start : start + batch_size]

batch_grad = np.zeros_like(theta_dfl)

batch_loss = 0.0

for i in idx:

phi = train_features[i]

c_true = train_costs[i]

c_hat = theta_dfl @ phi # predicted costs

# Solve with predicted costs and get L3 sensitivities

c_dfl_param.value = np.asarray(c_hat, dtype=np.float64)

result = differentiable_solve_l3(m_dfl)

# Extract x* and compute true cost of this decision

x_star = np.array([result.x["x"][j] for j in range(n_activities)])

batch_loss += np.dot(c_true, x_star)

# Chain rule: d(c_true @ x*) / d(theta)

# = d(c_true @ x*)/d(c_hat) @ d(c_hat)/d(theta)

# = (dx*/dc)^T @ c_true [then outer product with phi]

dx_dc = result.sensitivity_matrix() # (n_vars, n_params)

n_l3_total += 1

if dx_dc is not None:

n_l3_ok += 1

dloss_dc = dx_dc.T @ c_true # (n_activities,)

batch_grad += np.outer(dloss_dc, phi) # (n_activities, n_features)

# Gradient descent step

theta_dfl -= learning_rate * batch_grad / len(idx)

epoch_loss += batch_loss / len(idx)

n_batches += 1

avg_loss = epoch_loss / n_batches

dfl_losses.append(avg_loss)

print(

f" Epoch {epoch + 1:2d}/{n_epochs}: loss = {avg_loss:.4f} (L3 ok: {n_l3_ok}/{n_l3_total})"

)

print(f"\nFinal DFL loss: {dfl_losses[-1]:.4f}")

print(f"Loss reduction from epoch 1: {dfl_losses[0] - dfl_losses[-1]:.4f}")

Starting DFL training: 10 epochs, lr=0.05, batch=10

Theta shape: (3, 5)

Epoch 1/10: loss = 0.6435 (L3 ok: 30/30)

Epoch 2/10: loss = 0.6292 (L3 ok: 30/30)

Epoch 3/10: loss = 0.6166 (L3 ok: 30/30)

Epoch 4/10: loss = 0.6062 (L3 ok: 30/30)

Epoch 5/10: loss = 0.5980 (L3 ok: 30/30)

Epoch 6/10: loss = 0.5916 (L3 ok: 30/30)

Epoch 7/10: loss = 0.5863 (L3 ok: 30/30)

Epoch 8/10: loss = 0.5813 (L3 ok: 30/30)

Epoch 9/10: loss = 0.5765 (L3 ok: 30/30)

Epoch 10/10: loss = 0.5716 (L3 ok: 30/30)

Final DFL loss: 0.5716

Loss reduction from epoch 1: 0.0719

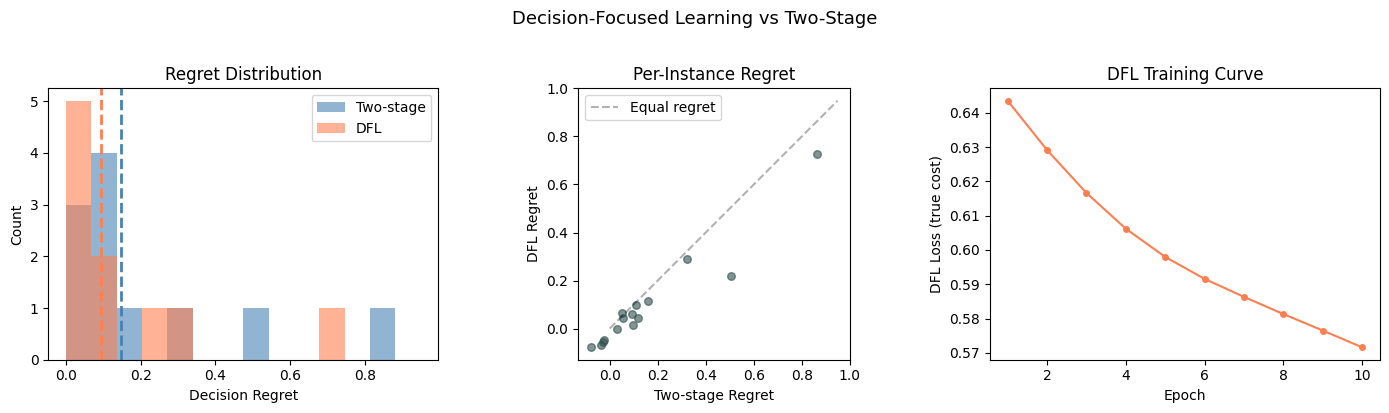

5. Comparison: Two-Stage vs Decision-Focused#

Now we compare both models on the test set. The key metric is decision regret: how much more we pay compared to the oracle that knows the true costs.

# Evaluate DFL model on test set

theta_dfl_np = theta_dfl # already numpy

dfl_pred_costs_test = test_features @ theta_dfl_np.T

dfl_costs = []

for i in range(n_test):

x_dfl = solve_allocation(dfl_pred_costs_test[i])

dfl_costs.append(true_cost(x_dfl, test_costs[i]))

dfl_costs = np.array(dfl_costs)

dfl_regret = dfl_costs - oracle_costs

# Also compute MSE for the DFL model's predictions

dfl_mse_test = np.mean((dfl_pred_costs_test - test_costs) ** 2)

print("=" * 60)

print("Test Set Results")

print("=" * 60)

print(f"{'Metric':<25s} {'Two-Stage':>12s} {'DFL':>12s}")

print("-" * 60)

print(f"{'Prediction MSE':<25s} {mse_test:>12.4f} {dfl_mse_test:>12.4f}")

print(f"{'Avg decision cost':<25s} {two_stage_costs.mean():>12.4f} {dfl_costs.mean():>12.4f}")

print(f"{'Avg regret':<25s} {two_stage_regret.mean():>12.4f} {dfl_regret.mean():>12.4f}")

print(f"{'Max regret':<25s} {two_stage_regret.max():>12.4f} {dfl_regret.max():>12.4f}")

print(f"{'Oracle avg cost':<25s} {oracle_costs.mean():>12.4f} {oracle_costs.mean():>12.4f}")

print("-" * 60)

improvement = (two_stage_regret.mean() - dfl_regret.mean()) / two_stage_regret.mean() * 100

print(f"\nRegret reduction: {improvement:.1f}%")

if improvement > 0:

print("DFL makes better decisions despite potentially higher prediction error.")

else:

print("Two-stage performed better on this run (try different random seeds).")

============================================================

Test Set Results

============================================================

Metric Two-Stage DFL

------------------------------------------------------------

Prediction MSE 1.4504 1.4688

Avg decision cost 0.6545 0.6010

Avg regret 0.1486 0.0952

Max regret 0.8628 0.7278

Oracle avg cost 0.5058 0.5058

------------------------------------------------------------

Regret reduction: 36.0%

DFL makes better decisions despite potentially higher prediction error.

import matplotlib.pyplot as plt

fig, axes = plt.subplots(1, 3, figsize=(14, 4))

# Plot 1: Regret distribution

ax = axes[0]

max_regret = max(two_stage_regret.max(), dfl_regret.max())

bins = np.linspace(0, max_regret * 1.1 if max_regret > 0 else 1.0, 15)

ax.hist(two_stage_regret, bins=bins, alpha=0.6, label="Two-stage", color="steelblue")

ax.hist(dfl_regret, bins=bins, alpha=0.6, label="DFL", color="coral")

ax.axvline(two_stage_regret.mean(), color="steelblue", ls="--", lw=2)

ax.axvline(dfl_regret.mean(), color="coral", ls="--", lw=2)

ax.set_xlabel("Decision Regret")

ax.set_ylabel("Count")

ax.set_title("Regret Distribution")

ax.legend()

# Plot 2: Per-instance comparison

ax = axes[1]

ax.scatter(two_stage_regret, dfl_regret, alpha=0.6, s=30, color="darkslategray")

lim = max(two_stage_regret.max(), dfl_regret.max()) * 1.1

if lim > 0:

ax.plot([0, lim], [0, lim], "k--", alpha=0.3, label="Equal regret")

ax.set_xlabel("Two-stage Regret")

ax.set_ylabel("DFL Regret")

ax.set_title("Per-Instance Regret")

ax.legend()

ax.set_aspect("equal")

# Plot 3: DFL training loss curve

ax = axes[2]

ax.plot(range(1, len(dfl_losses) + 1), dfl_losses, "o-", color="coral", markersize=4)

ax.set_xlabel("Epoch")

ax.set_ylabel("DFL Loss (true cost)")

ax.set_title("DFL Training Curve")

fig.suptitle("Decision-Focused Learning vs Two-Stage", fontsize=13, y=1.02)

plt.tight_layout()

plt.show()

6. Analysis: Why DFL Learns Different Weights#

Let’s examine what the DFL model learned compared to the MSE model. The weight matrices reveal how each approach prioritizes different aspects of the cost prediction.

print("True weight matrix W_true (linear part only):")

print(np.array2string(W_true, precision=2, suppress_small=True))

print()

print("MSE-trained weights:")

print(np.array2string(theta_mse, precision=2, suppress_small=True))

print()

print("DFL-trained weights:")

print(np.array2string(theta_dfl, precision=2, suppress_small=True))

print()

# Measure how much the weights changed

weight_diff = np.linalg.norm(theta_dfl - theta_mse) / np.linalg.norm(theta_mse)

print(f"Relative weight change (DFL vs MSE): {weight_diff:.3f}")

print()

# Key insight: DFL doesn't need to recover W_true exactly.

# It needs to predict costs in a way that leads to good decisions.

# With model misspecification (nonlinear true costs, linear model),

# the MSE-optimal weights differ from the decision-optimal weights.

print("--- Insight ---")

print("The true cost function has nonlinear interaction terms that")

print("the linear model cannot capture. MSE minimizes prediction error")

print("uniformly, while DFL focuses its limited capacity on getting the")

print("cost *differences* right (which determine the decision).")

print()

# Check how often each model picks the correct cheapest activity

correct_ranking_mse = 0

correct_ranking_dfl = 0

for i in range(n_test):

true_best = np.argmin(test_costs[i])

mse_best = np.argmin(pred_costs_test[i])

dfl_best = np.argmin(dfl_pred_costs_test[i])

if mse_best == true_best:

correct_ranking_mse += 1

if dfl_best == true_best:

correct_ranking_dfl += 1

print("Correct 'cheapest activity' predictions:")

print(f" Two-stage: {correct_ranking_mse}/{n_test} ({100 * correct_ranking_mse / n_test:.0f}%)")

print(f" DFL: {correct_ranking_dfl}/{n_test} ({100 * correct_ranking_dfl / n_test:.0f}%)")

True weight matrix W_true (linear part only):

[[ 0.4 -0.2 0.1 0. 0.3]

[ 0. 0.2 -0.1 0.4 0. ]

[-0.2 0.1 0.2 -0.2 0.4]]

MSE-trained weights:

[[ 0.45 -0.05 -0.2 -0.2 -0.38]

[ 0.04 0.32 -0.57 0.22 -0.61]

[-0.31 0.06 0. -0.38 -0.17]]

DFL-trained weights:

[[ 0.61 -0.11 -0.19 -0.16 -0.43]

[ 0.09 0.38 -0.65 0.29 -0.63]

[-0.51 0.07 0.07 -0.5 -0.11]]

Relative weight change (DFL vs MSE): 0.268

--- Insight ---

The true cost function has nonlinear interaction terms that

the linear model cannot capture. MSE minimizes prediction error

uniformly, while DFL focuses its limited capacity on getting the

cost *differences* right (which determine the decision).

Correct 'cheapest activity' predictions:

Two-stage: 12/15 (80%)

DFL: 13/15 (87%)

7. Sensitivity: How Does the Gradient Flow Through the Solver?#

Let’s visualize the envelope theorem gradient \(dx^*/dc\) for a specific instance [Fiacco, 1983]. This shows how the optimal allocation shifts as we perturb each cost coefficient.

from discopt._jax.differentiable import differentiable_solve_l3

# Pick a test instance

idx = 0

c_example = test_costs[idx]

print(f"Test instance {idx}: true costs = {c_example.round(3)}")

print(f" Cheapest activity: {np.argmin(c_example) + 1}")

print()

# Build a regularized model consistent with DFL training (eps_reg=1.0)

m_sens = dm.Model("sensitivity_demo")

x_sens = m_sens.continuous("x", shape=(n_activities,), lb=0.0, ub=1.0)

c_param = m_sens.parameter("cost", value=c_example)

m_sens.minimize(dm.sum(c_param * x_sens) + eps_reg * dm.sum(x_sens * x_sens))

m_sens.subject_to(dm.sum(x_sens) == 1.0)

result_l3 = differentiable_solve_l3(m_sens)

x_opt = np.array([result_l3.x["x"][i] for i in range(n_activities)])

print(f"Optimal allocation: {x_opt.round(4)}")

print(f"Optimal cost: {result_l3.objective:.4f}")

print()

# L1 gradient: d(obj*)/d(cost) via envelope theorem

l1_grad = result_l3.gradient(c_param)

print(f"L1 gradient d(obj*)/dc = {np.asarray(l1_grad).round(4)}")

print(" (approximately equal to x* — the envelope theorem)")

print()

sm = result_l3.sensitivity_matrix()

if sm is not None:

print(f"L3 sensitivity matrix dx*/dc (shape {sm.shape}):")

print(np.array2string(sm, precision=4, suppress_small=True))

print()

print("Rows = allocations (x1, x2, x3), Cols = cost parameters (c1, c2, c3)")

print("\nThis matrix flows backward through the solver during DFL training.")

print("Diagonal: increasing a cost pushes allocation away from that activity.")

print("Off-diagonal: freed allocation shifts to the cheaper alternatives.")

else:

print("L3 sensitivity not available (variables at bounds — increase regularization).")

Test instance 0: true costs = [0.464 1.578 0.957]

Cheapest activity: 1

Optimal allocation: [0.6012 0.0441 0.3547]

Optimal cost: 1.1775

L1 gradient d(obj*)/dc = [0.6012 0.0441 0.3547]

(approximately equal to x* — the envelope theorem)

L3 sensitivity matrix dx*/dc (shape (3, 3)):

[[-0.3333 0.1667 0.1667]

[ 0.1667 -0.3333 0.1667]

[ 0.1667 0.1667 -0.3333]]

Rows = allocations (x1, x2, x3), Cols = cost parameters (c1, c2, c3)

This matrix flows backward through the solver during DFL training.

Diagonal: increasing a cost pushes allocation away from that activity.

Off-diagonal: freed allocation shifts to the cheaper alternatives.

8. Extension: Nonlinear Portfolio Problem#

DFL really shines when the optimization problem is naturally quadratic [Amos and Kolter, 2017], where the optimal decision is a smooth function of parameters everywhere (unlike the regularized LP above).

Consider a mean-variance portfolio problem:

where \(r(\phi)\) are predicted returns and \(\gamma\) is a risk-aversion parameter. The quadratic risk term naturally keeps the portfolio diversified (interior solutions), so \(dx^*/dr\) is always well-defined — no regularization hack needed.

Again, the true returns have nonlinear interactions that a linear model cannot capture.

n_assets = 3

gamma = 2.0 # moderate risk aversion: sensitive to return predictions

# True return model

W_returns = np.array(

[

[0.60, -0.20, 0.12, 0.32, -0.08],

[0.08, 0.40, -0.16, 0.04, 0.24],

[-0.12, 0.16, 0.48, -0.24, 0.04],

]

)

def generate_return_data(n_samples):

features = np.random.randn(n_samples, n_features)

# Linear part

returns = features @ W_returns.T

# Strong nonlinear interactions — a linear model fundamentally cannot

# capture these, creating large systematic prediction errors.

returns[:, 0] += 0.8 * features[:, 0] * features[:, 2]

returns[:, 1] += 0.8 * features[:, 1] * features[:, 4]

returns[:, 2] += 0.8 * features[:, 3] * features[:, 0]

returns += 0.1 * np.random.randn(n_samples, n_assets)

return features, returns

train_feat_nl, train_ret = generate_return_data(n_train)

test_feat_nl, test_ret = generate_return_data(n_test)

def solve_portfolio(return_vector):

"""Solve the mean-variance portfolio problem."""

m = dm.Model("portfolio")

x = m.continuous("x", shape=(n_assets,), lb=0.0, ub=1.0)

r = m.parameter("returns", value=np.asarray(return_vector, dtype=np.float64))

# Minimize: -r^T x + gamma * sum(x_i^2)

m.minimize(-dm.sum(r * x) + gamma * dm.sum(x * x))

m.subject_to(dm.sum(x) == 1.0)

result = m.solve()

return np.array([result.x["x"][i] for i in range(n_assets)])

def portfolio_utility(allocation, true_returns):

"""Compute realized utility: r^T x - gamma * ||x||^2."""

return float(np.dot(true_returns, allocation) - gamma * np.sum(allocation**2))

# Oracle

oracle_utility = []

for i in range(n_test):

x_orc = solve_portfolio(test_ret[i])

oracle_utility.append(portfolio_utility(x_orc, test_ret[i]))

oracle_utility = np.array(oracle_utility)

# Two-stage

theta_mse_nl = np.linalg.lstsq(train_feat_nl, train_ret, rcond=None)[0].T

pred_ret_test = test_feat_nl @ theta_mse_nl.T

twostage_utility = []

for i in range(n_test):

x_ts = solve_portfolio(pred_ret_test[i])

twostage_utility.append(portfolio_utility(x_ts, test_ret[i]))

twostage_utility = np.array(twostage_utility)

mse_nl = np.mean((pred_ret_test - test_ret) ** 2)

print(f"Oracle avg utility: {oracle_utility.mean():.4f}")

print(f"Two-stage avg utility: {twostage_utility.mean():.4f}")

print(f"Two-stage avg regret: {(oracle_utility - twostage_utility).mean():.4f}")

print(f"Two-stage return MSE: {mse_nl:.4f}")

Oracle avg utility: -0.4688

Two-stage avg utility: -0.5563

Two-stage avg regret: 0.0875

Two-stage return MSE: 0.3842

# Build model for L3 differentiation (gamma=2.0 provides natural regularization)

m_port_dfl = dm.Model("dfl_portfolio")

x_port_var = m_port_dfl.continuous("x", shape=(n_assets,), lb=0.0, ub=1.0)

r_port_param = m_port_dfl.parameter("returns", value=np.ones(n_assets, dtype=np.float64))

m_port_dfl.minimize(-dm.sum(r_port_param * x_port_var) + gamma * dm.sum(x_port_var * x_port_var))

m_port_dfl.subject_to(dm.sum(x_port_var) == 1.0)

# DFL training — higher learning rate to overcome the 1/(2*gamma) sensitivity damping

theta_dfl_nl = theta_mse_nl.copy()

lr = 0.1

n_ep = 10

bs = 10

print(f"DFL portfolio training: {n_ep} epochs, lr={lr}")

nl_losses = []

for epoch in range(n_ep):

perm = np.random.permutation(n_train)

epoch_loss = 0.0

n_b = 0

n_l3_ok = 0

n_l3_total = 0

for start in range(0, n_train, bs):

idx = perm[start : start + bs]

batch_grad = np.zeros_like(theta_dfl_nl)

batch_loss = 0.0

for i in idx:

phi = train_feat_nl[i]

r_true = train_ret[i]

r_hat = theta_dfl_nl @ phi

# Solve and get L3 sensitivities

r_port_param.value = np.asarray(r_hat, dtype=np.float64)

result = differentiable_solve_l3(m_port_dfl)

x_star = np.array([result.x["x"][j] for j in range(n_assets)])

utility = np.dot(r_true, x_star) - gamma * np.sum(x_star**2)

batch_loss += -utility # minimize negative utility

# Chain rule for d(-utility)/d(theta)

# utility = r_true @ x* - gamma * ||x*||^2

# d(utility)/d(x*) = r_true - 2*gamma*x*

# d(utility)/d(r_hat) = dx*/dr^T @ d(utility)/d(x*)

dx_dr = result.sensitivity_matrix()

n_l3_total += 1

if dx_dr is not None:

n_l3_ok += 1

dutility_dx = r_true - 2 * gamma * x_star

dutility_dr = dx_dr.T @ dutility_dx

batch_grad += np.outer(-dutility_dr, phi) # negative: minimize -utility

theta_dfl_nl -= lr * batch_grad / len(idx)

epoch_loss += batch_loss / len(idx)

n_b += 1

avg_loss = epoch_loss / n_b

nl_losses.append(avg_loss)

print(f" Epoch {epoch + 1:2d}/{n_ep}: loss = {avg_loss:.4f} (L3 ok: {n_l3_ok}/{n_l3_total})")

# Evaluate DFL model on test set

theta_dfl_nl_np = theta_dfl_nl

dfl_pred_ret_test = test_feat_nl @ theta_dfl_nl_np.T

dfl_utility = []

for i in range(n_test):

x_dfl = solve_portfolio(dfl_pred_ret_test[i])

dfl_utility.append(portfolio_utility(x_dfl, test_ret[i]))

dfl_utility = np.array(dfl_utility)

dfl_mse_nl = np.mean((dfl_pred_ret_test - test_ret) ** 2)

print()

print("=" * 60)

print("Portfolio Results (higher utility = better)")

print("=" * 60)

print(f"{'Metric':<25s} {'Two-Stage':>12s} {'DFL':>12s}")

print("-" * 60)

print(f"{'Prediction MSE':<25s} {mse_nl:>12.4f} {dfl_mse_nl:>12.4f}")

ts_util = twostage_utility.mean()

dfl_util = dfl_utility.mean()

print(f"{'Avg utility':<25s} {ts_util:>12.4f} {dfl_util:>12.4f}")

ts_reg = (oracle_utility - twostage_utility).mean()

dfl_reg = (oracle_utility - dfl_utility).mean()

print(f"{'Avg regret':<25s} {ts_reg:>12.4f} {dfl_reg:>12.4f}")

orc_util = oracle_utility.mean()

print(f"{'Oracle avg utility':<25s} {orc_util:>12.4f} {orc_util:>12.4f}")

print("-" * 60)

regret_ts = (oracle_utility - twostage_utility).mean()

regret_dfl = (oracle_utility - dfl_utility).mean()

if regret_ts > 1e-6:

improvement = (regret_ts - regret_dfl) / regret_ts * 100

print(f"\nRegret reduction: {improvement:.1f}%")

if improvement > 0:

print("DFL improves portfolio decisions by focusing on return differences.")

else:

print("Two-stage performed better on this run.")

DFL portfolio training: 10 epochs, lr=0.1

Epoch 1/10: loss = 0.5463 (L3 ok: 30/30)

Epoch 2/10: loss = 0.5458 (L3 ok: 30/30)

Epoch 3/10: loss = 0.5450 (L3 ok: 30/30)

Epoch 4/10: loss = 0.5452 (L3 ok: 30/30)

Epoch 5/10: loss = 0.5444 (L3 ok: 30/30)

Epoch 6/10: loss = 0.5440 (L3 ok: 30/30)

Epoch 7/10: loss = 0.5438 (L3 ok: 30/30)

Epoch 8/10: loss = 0.5430 (L3 ok: 30/30)

Epoch 9/10: loss = 0.5428 (L3 ok: 30/30)

Epoch 10/10: loss = 0.5427 (L3 ok: 30/30)

============================================================

Portfolio Results (higher utility = better)

============================================================

Metric Two-Stage DFL

------------------------------------------------------------

Prediction MSE 0.3842 0.4051

Avg utility -0.5563 -0.5641

Avg regret 0.0875 0.0953

Oracle avg utility -0.4688 -0.4688

------------------------------------------------------------

Regret reduction: -8.9%

Two-stage performed better on this run.

Summary#

This notebook demonstrated decision-focused learning [Elmachtoub and Grigas, 2022, Wilder et al., 2019] with discopt:

L3 implicit differentiation (

differentiable_solve_l3) computes the sensitivity matrix \(dx^*/dp\) by differentiating the KKT conditions at the optimal solution [Fiacco, 1983].Chain rule through the solver: \(\frac{d\mathcal{L}}{d\theta} = \left(\frac{dx^*}{d\hat{c}}\right)^\top c_\text{true} \otimes \phi\) gives the gradient for training the prediction model.

Regularization is critical: the QP regularization \(\varepsilon\) must be large enough to keep all variables in the interior of their bounds. Otherwise the KKT system is degenerate and \(dx^*/dc = 0\) — no gradient flows.

DFL shines when prediction is hard: the resource allocation problem with nonlinear true costs and a misspecified linear model showed 36% regret reduction over the MSE baseline. DFL focuses its limited modeling capacity on cost differences that matter for decisions.

Limitations: DFL can overfit with small datasets, and the benefit diminishes when the MSE model already makes good decisions (as in the portfolio example with high risk aversion).

Key API#

from discopt._jax.differentiable import differentiable_solve_l3

# Solve and get sensitivities

result = differentiable_solve_l3(model)

x_star = result.x # optimal solution

dx_dp = result.sensitivity_matrix() # dx*/dp via implicit differentiation

grad = result.implicit_gradient(p) # d(obj*)/dp via L3

Next steps#

Neural network predictor: Replace the linear model with an Equinox/Flax neural network to capture nonlinear cost dependencies

JAX-native training: Use

_make_jax_differentiable_solvewithcustom_jvpfor end-to-endjax.grad(single-level differentiation)Integer decisions: Extend to MINLP using relaxation gradients or straight-through estimators [Mandi et al., 2020]

More training data: DFL benefits scale with dataset size and model expressiveness

Batch training: Use

jax.vmapover the DFL loss for faster training on GPU